Investing With "Play Money"

Around the time baby girl was born, a company called Lending Loop received approvals from Canadian regulators to open up shop again. The primary business model of Lending Loop is to lend money out to businesses using money from members. It's actually very similar to the banking model, except with Lending Loop the members choose who to loan money too and the members reap most of the rewards (minus a small fee paid to Lending Loop). In other words, it's more like a peer-to-peer loan. In addition to that, all the research and due diligence is done by Lending Loop and they and the business work out an agreement in terms of principal, interest rate, and length of term.

At the time, I still had $200 in my Paypal account from selling some of my unused Magic cards. Rather than have that money sit in the account earning nothing, why not just throw the money into Lending Loop and give it a shot? I decided that this $200, would be considered my "play money". As the money wasn't doing anything in particular, I wouldn't really miss it if Lending Loop were to collapse the next day and take my $200 investment with them. While I could have put that money into my investment account and bought some individual stocks with this "play money", $200 isn't a lot of money and to buy individual stocks in my Questrade account will cost between $4.95 to $9.95 per transaction. There's also no need to buy individual stocks as the index ETFs already hold most of the available stocks in North America and around the globe. Aside from the fees that are paid to Lending Loop when you receive loan repayments, there are no up front costs to having an account in Lending Loop.

The transfer of the money from Paypal to Tangerine and then Tangerine to Lending Loop took almost a week to complete. Once the money was transferred and ready, I looked through the available loans in the Lending Loop Marketplace.

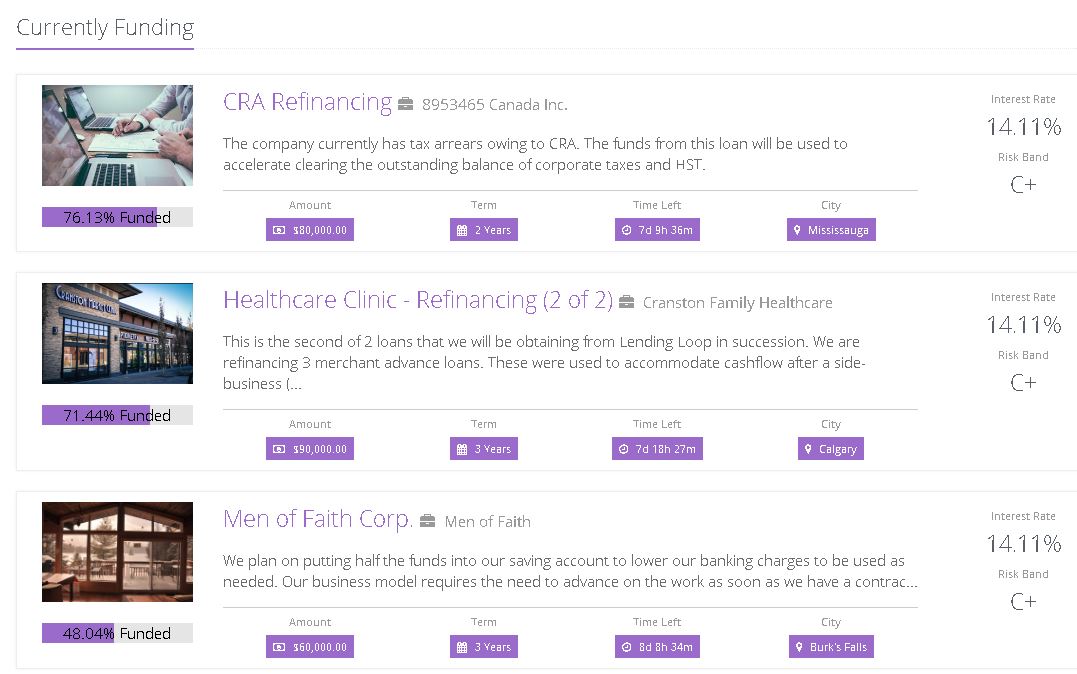

At the time, there weren't many options available as Lending Loop had just started. However, currently, there are 5 different loans looking to be funded and another 5 just completed funding and looking to be finalized. From this list, you can see the risk level, interest rate, amount, and term. You can also click on a company to find out about their reasons for the loan, their financial statements, project payment schedule, and even business details. There is also an option for you to ask questions regarding their business. The following is one of the companies listed as a B risk customer.

Once you find a company to loan money to, you just have to enter the amount you want to loan (minimum $25 and in increments of $25) and that's it! It's very simple.

As you would expect, the loans with a risk factor of A are funded pretty quickly and usually carry an interest rate of 8% or so. Loans with a D risk factor are riskier but usually come with a much higher rate. I have loaned $50 to one D risk factor company and the interest rate is 20%!

7 months in and there already has been one repaid loan. On my initial $200 and through funding 6 loans, I've earned $11.45. Doesn't sound very impressive, but doing some math, the current interest rate is 9.8%! Which isn't too bad. I still have $18 or so sitting in my account, but still need $7 until I can pledge my money towards another loan.

Is there a risk of some or all of these loans defaulting? Definitely. The only safe methods to "invest" are with a GIC or High Interest Savings Account. However, these two methods actually lose out to inflation.

However, that's why it was important for me to not miss this $200. In the grand scheme of things, $200 as a percentage of our total cash and investments is less that 0.1%. The stock market fluctuations are more than $200 each day. Yesterday, our portfolio went down 0.3% or so.

There are some people who suggest 10% of your portfolio if you absolutely need to "play" (or gamble) with your investments. I'm not comfortable putting $24,000 at risk. Nor am I comfortable with "playing" with $2,400. However, $200, is an amount I can live with.

Overall, I've been happy with how my "play money" has performed thus far. Even if it's only enough money for lunch takeout for two.

Comments

Post a Comment