Variable Winds? Channel It In One Direction Instead

|

| How do you spend $20,000 a year in travel? |

A while back, I read an article about a young couple looking to retire early at the age of 55. The newspaper enlisted the help of a financial planner and went through many scenarios to see if the couple could retire when they wanted with the annual spending goal (inflation adjusted) of $106,000 a year, after tax, and an additional $29,000 for traveling.

Holy cow.

$135,000 a year after taxes. Assuming an even split of income, that's around $87,000 each before taxes.

The woman actually has a pension plan that would pay around $56,000 a year from 55 with a bridge benefit of $8,000 or so until 65. So assuming she works for another 22 years, they need to figure out a way to earn an additional $118,000 a year. Even assuming a higher pension, this couple still needs to figure out how they can earn another $98,000 a year in retirement.

However, when the financial planner runs the math, it doesn't quite add up. This couple, despite bringing home $8,000 a month will be short of their retirement goals.

Why is that?

Well, the financial planner gets right to the heart of the problem. In each scenario, he presents them with another amount they need to spend in retirement or the amount they need to save additionally each year to make their current goals sustainable.

It's not pretty.

In one scenario, they have to cut their retirement spending to $52,000 or save an additional $23,000 a year. Ouch.

Can you imagine? Instead of spending $135,000 after taxes, you can only spend $52,000?! What kind of financial planner is this?

Judging from the article, a realistic one.

Going through their expenses at the end, this couple has a savings rate of 21% ($1,692 savings from $8,000 of take home pay). Though, I'm not sure why they list RRSP, TFSA, and RESP as expenses. It's their article, they can do whatever they want. It just makes the couple look like they have a shortfall, but they don't.

Now, that savings rate is pretty good. It could be better.

First thing that can be done that pops right out (at least for me), sell the second property. Sure they are breaking even. Great. What happens when the tenant moves out and the place is left vacant for months at a time?

What happens when the tenant leaves and they discover the rental property requires thousands of dollars for repairs?

For me, the best thing to do would be to sell it. I'm going to assume they can sell the property for what it's worth and have $400,000 left over after fees and commissions.

As they have to put 20% down on the property, let's just assume they paid $300,000 for the rental property. They'll need to pay taxes on the $130,000 in capital gains. Only 50% of realized capital gains are taxed, then assuming a top marginal tax rate of 50%, that leaves them with $367,500. After paying off the second mortgage, that's $127,500 they can throw into their own mortgage.

Let's assume the fees to break the mortgage are insane. So that takes away their $127,500 + $17,500 in their TFSA. But now they are mortgage free!

That frees up $1,695 a month!

I've essentially doubled their savings rate from 21% to 42% ($3,387 of $8,000).

Digging into their expenses, they spend $600 a month for groceries AND $600 a month for dining out and entertainment.

Just wow. $1,200 a month for food for two people and a baby.

Just cutting this amount in half and we'll have an additional $600 a month to save. The savings rate is now almost 50% at 49.8% ($3,987 of $8,000).

This couple also has a car loan of $11,000 and $11,500 cash in the bank. Uh... okay. They are paying $350 a month towards this car loan. That's just bad. If they take the money from the bank and pay off the car loan, they'll have $500 left in the bank. However, now they are saving $4,337 a month. They'll be able to replenish their bank account in 3 months!

At $4,337 of savings a month, their savings rate will be 54%.

There's still more.

The article indicates this couple is spending $280 a month on TV, phones and internet. Wifey and I are spending $135 a month for phones (mobile phones and home phone) and internet. We've cut the cable as we no longer have time to watch TV.

Assuming this couple can cut these expenses to around $140 a month, that's a total of $4,477 of savings a month!

Bam! Just like that, they have savings rate of 56%, they are mortgage free, they no longer have a car loan, and will definitely have more time to spend with their kid (and making a second one as that is listed as one of their goals).

Not only that, but I've cut their expenses from $75,696 a year to $42,276.

In a few years when they no longer need child care, they'll have an additional $1,200 a year in savings. Or yearly expenses of $27,876.

|

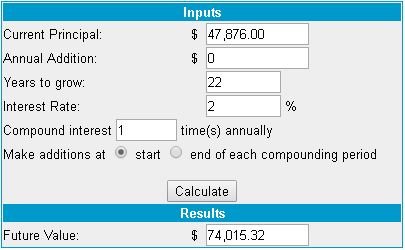

| Calculation of expenses after inflation in 22 years. This amount includes the $20,000 a year for travel. |

So in retirement, they won't need $135,000 after tax to live their lives. They'll only need $47,876 in today's dollars or $74,015 a year after tax in 22 years (assuming 2% inflation).

So how much will this couple have if they banked all their savings in index funds that generate an annual return for 5.5% (the estimate in the article)?

With only one kid, they'll have over $2.3M by the time they are 55.

|

| Calculation of financial assets with one kid after 22 years. |

With two kids, they'll have over $1.7M.

|

| Calculation of financial assets with two kids after 22 years. |

My calculations are flawed though. I'm assuming they'll be paying $1,200 and $2,400 every month for the entirely of 22 years for child care expenses. It would be complicated to estimate when they no longer need to pay for child care, so I'm just going to leave it.

Either way, they'll have more than enough financial assets to live the retirement they want if they implemented the measures I suggested.

Comments

Post a Comment